The Millennial's Guide To Saving For A Down Payment (...or a wedding... or a vacation ... orrr)

how to save up for a downpayment: the millenial’s guide to saving money… without even thinking about it

Let me just say this—I take my finances very seriously, and I think you should too.

Money is absolutely imperative in living your most vibrant life. In recent years I’ve done a lot of work on abundance mindset—giving gratitude to money for allowing me to feel secure and free. Secure enough to know that we have enough to cover the basics and live, and free in the fact that we can afford extra things that make us happy: a quality face mask, date nights out, a delicious bottle of wine, a cozy sweater…

But what about saving for the BIG STUFF?! Down payments, weddings, student loans, travel… Now that feels a little bit more intense and scary.

But it doesn’t have to be.

This blog post is dedicated to showing you exactly how Adam and I saved up for our down payment (and our wedding…and my grad school tuition) with a combined household income of less than 100K.

I pinkie promise that I will not tell you never to buy a shirt again or that you can’t go out to eat for a year. Instead, this blog post is a REALISTIC millennial’s guide to putting your money where your mouth is. This is my secret formula of saving up for big things. And it’s quite easy! Giddy up!

step one: let’s start at the very beginning…

This is how any good adventure starts—with research. This step is allllll about sitting down and calculating monthly expenses. Let me just start this out by saying that I think this is a GREAT exercise for anyone, not just if you’re looking at buying a house, planning a wedding, or saving for something BIG.

While it may seem intimidating to sit down and get a good look at your finances, you’ll likely end up feeling so much freedom when you really break down where your money is going + know how to move forward.

Now this isn’t a budget per se, but this is where we estimated allllllllll of our monthly expenses—no matter how big or small, we wanted to see where we were at in terms of money in and money out. When we started the home search process, this is how detailed we got when realistically planning our budget, and you will be shocked by how much detail we went in to. This memory is always funny to me because we were debating if we were *ready* to buy a house so we literally crammed together in a tiny bath tub of our first apartment, poured a glass of wine, and sat in a bubble bath while compiling our monthly expenses #adulting.

START HERE:

Monthly income (after taxes are taken out):

Spouse’s income (after taxes are taken out):

Any other side income (average):

TOTAL MONTHLY INCOME:

THEN CALCULATE MONTHLY EXPENSES:

-Mortgage/rent

-Retirement

-Emergency fund

-Health/dental

-Savings

-Credit card payment

-Clothing

-Car payment

-Car insurance

-Car maintenance

-Gas

-Groceries

-Phone bill

-Netflix/Hulu

-Dining out

-Clothing

-Home expenses

-Beer/wine

-Coffee

-Gym membership

-Haircuts

-Pet expenses (food, grooming, etc)

-Money for Christmas, birthdays, wedding gifts, etc.

(Expenses to Add if You’re Considering a House):

-Property taxes

-Home insurance

-Electricity

-Garbage bill

-Neighborhood dues

-Home renovation costs

-Snowplow (for all my Midwest peeps!)

-Lawn mower

TOTAL EXPENSES:

Then, what you’ll do:

TOTAL MONTHLY INCOME - TOTAL MONTHLY EXPENSES = LEFTOVER MONEY

This is a powerful exercise because you might have an idea of what you’re spending each month, but when you truly look at money in versus money out with cold, hard math, you’ll see a clear picture of your financial health. You will see immediately if what you earn is adequate enough to cover these costs or not. If you end up with a negative number, you know that you've got to make some adjustments. Basically: if that leftover money isn’t as high as you’d like it to be—where can you adjust?

step two: purchase mindfully

After looking at your financial situation you may be thinking “OMG, I’ll never be able to afford [fill in the blank]!”

But LOOK at where you are currently spending your money. For me and Adam, it was saying WHOA to how much we spent at restaurants. Let me just say that we loooove going out to eat—but we took it a bit too far. When we first graduated college and had a “big kid” salary, we went out to eat allllll the time. Like 3 date nights a week type thing. Silly! When we looked at our expenses, we realized we could literally save hundreds of dollars a month just by evolving to one date night per week. For us, that was a good trade off! I also had to look closely at my clothing purchases (which was actually my first ever step in creating a capsule wardrobe). Overall, it was small little tweaks we made to ensure that our “leftover” money was sufficient.

This is where you can transform your spending: stop buying mindlessly. Why do you keep spending $8 a day in a work cafeteria when you could pack a salad for $2? Why are you paying for that one monthly app subscription that you never use? Do you ever look at a charge on your bank statement and think, “I don’t even remember what that purchase was????” Chances are, whatever it was probably wasn’t worth it if it wasn’t worth remembering. It is truly in tweaking these little purchases that you can transform your finances.

To be honest, I never used to think about what I purchased—I would buy a $4 shirt off the clearance rack just because it was cheap and decently cute. I used to focus so much on how cheap something was that I didn’t even really think about what it was. Over time, I would buy maybe 25 individual $4 shirts that I would NEVER wear, when I could’ve spent that $100 dollars on 2–3 items that I loved. It ends up being the same amount of money, but you’re left with clutter and 25 shirts that you “kind of” like… no, thanks. I’ve learned to truly invest in where I put my dollar—not buying something unless I am utterly obsessed with it and it makes sense financially.

Things that will always be worth investing in to me: Nourishing, quality food. Travel. A pair of jeans that is flattering, ethically made, and built to last. A piece of art that is perfect for that little nook on the wall…

Spending mindfully doesn’t mean never buying something “fun” again, it means truly prioritizing, budgeting, and investing in where your money goes. General rule: if you can’t stop thinking about it, it’s probably a good investment that you’ll use again and again.

My parents were open with us about finances in little ways which never made it feel like a taboo topic. At a young age, I learned to say “I can’t afford that right now,” or “I’d rather spend my money on…,” which helped me be aware of the power, prioritization, and true gift that money is. Because when ya boil it down, money is just a tool that allows you to live your most vibrant life: investing in nourishing food, a home that makes you smile, a cozy date night, your wedding day, your education—you name it, money allows us to “do” it—and I think we should treat money with respect.

step three: assess your options (... and then live below your means)

Now that you’ve sat down and crunched the numbers and worked on mindfully spending, it’s time to look into how much you can spend on a house. NOTE: I don’t necessarily mean how much you are “approved” for. Adam and I were shocked at how much money for a mortgage we were approved for. Had we taken the max amount, we would be living paycheck-to-paycheck for 30 years. This is my blatant reminder that just because the bank tells you that you can afford a $400,000 house, does not mean it is wise financially. Remember, banks are a business—the higher loan you take out, the more money they make in interest.

For us, we ended up buying a house that was $150K less than what we were approved for. WOWZA. We wanted our house to be something we loved and felt relaxed in—not something that we were stressed about paying for month after month.

Once you have an amount for a house that you think you could comfortably afford, calculate your down payment. What’s recommended is having a down payment that is 20% of your home cost. Example: if you want to buy a house that is $150,000, you would take 150,000 x 0.2 = your downpayment of $30,000. You don’t need this amount by any means, but it makes things a whole lot cheaper in the long run! Just food for thought!

While this step is focused on future homeowners and how expensive of a house they can buy, the same goes for your wedding, vacation, whatever you are saving for. Look realistically at how much you can afford, and then try to shoot a little below that to make sure you feel comfortable and secure in your purchase. I promise, you’ll enjoy something a lotttt more if you’re not constantly stressed about how much it cost you

step four: my best-kept financial secret…

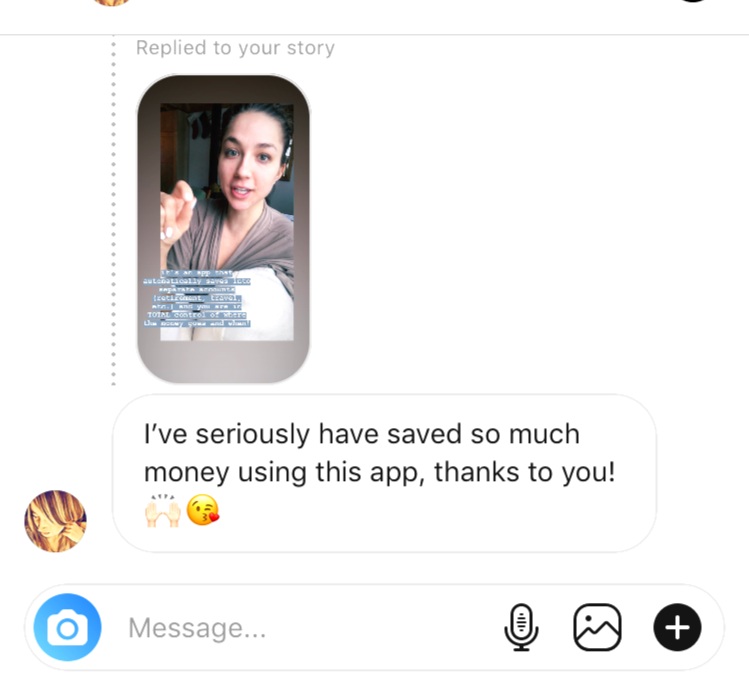

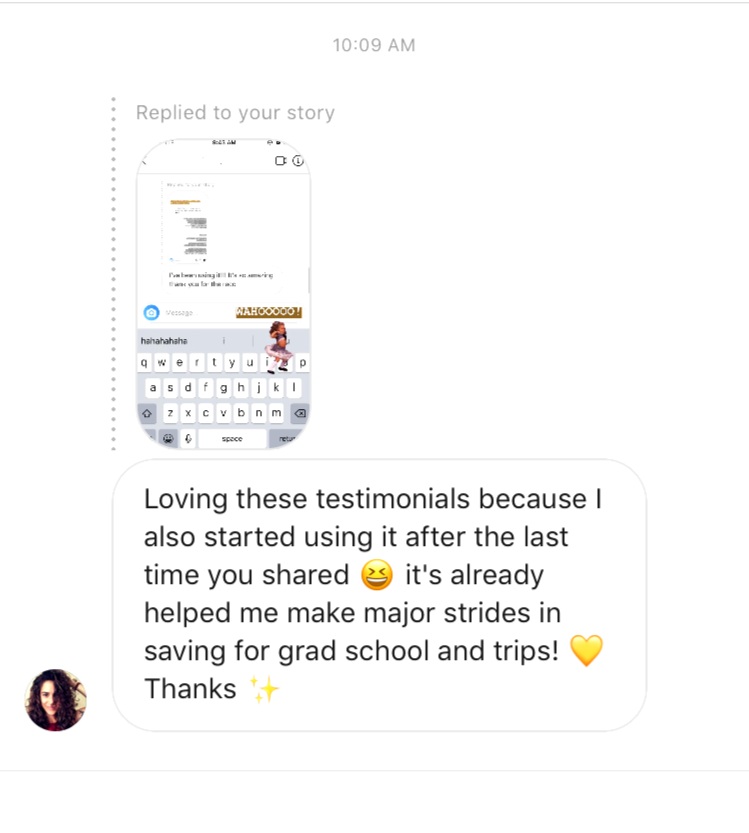

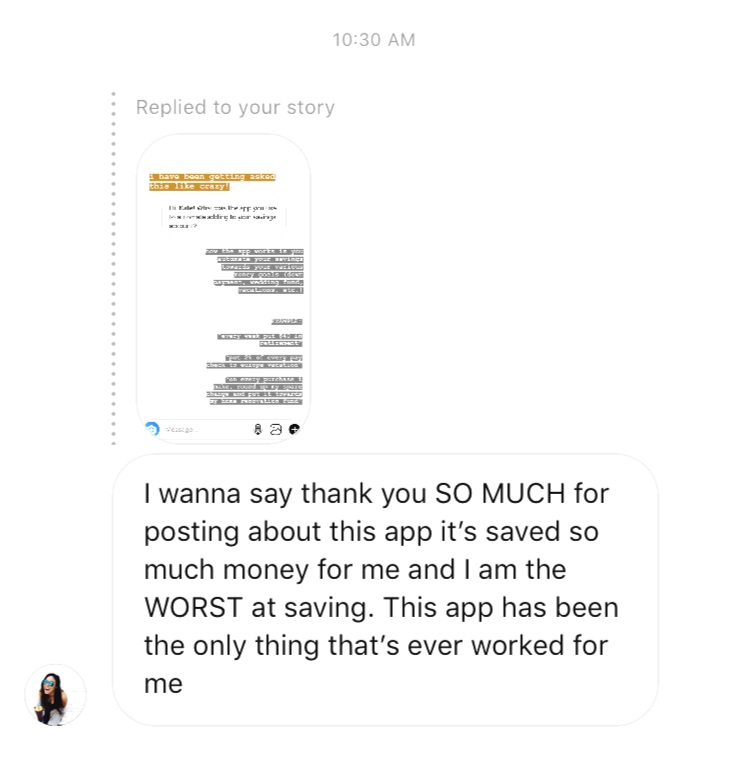

Ahhhh, my favorite step! OK, so here is where I reveal my secret to how to save up for your purchase. I found this savings app when I was in college and it was GAME CHANGING. Qapital is an app that allows you to set savings goals for anything : trip to Australia, concert tickets, retirement—you name it, and the app automatically starts saving for you. SAY WHAAA? I went from having quite literally $0 in savings to thousands in just a few months (….without even really thinking about it.)

Adam and I use it for everything—both big and small. We used it to save for our wedding, down payment, every single trip we take, and even the smaller purchases we want like a Vitamix or closet doors (yes, really).

HOW IT WORKS: Once you download the app, you customize what you’re saving for (wedding, down payment, Hawaii, etc.), set the amount of money you want to save for that goal, and customize how you would like to save towards it, thennnn (DRUM ROLL), the app will automatically start saving from your bank account, and you just sit back and watch your money pile growwww. :) if you are interested in trying qapital, use this link (or enter the code jq9657yh), and you’ll get $5 - $25 in your qapital account fo’ free to jumpstart your savings!

EXAMPLES OF HOW I HAVE SAVED WITH QAPITAL:

DOWN PAYMENT: $20,000

4% of each paycheck

$50 every Monday

Round up my spare change every time I swipe my card

VITAMIX BLENDER: $300

$10 every week

HAWAII VACATION: $2800

2% of paycheck

52-week rule: (save $1 on week 1, 2$ week 2, and so on for 52 weeks)

GRAD SCHOOL SPRING TUITION: $9000

$3 every day

6% of each paycheck

The beauty of this app is that it’s all automatic. I don’t know about you, but if there’s money chillin’ in my bank account I’ll likely just spend it on something silly. Qapital has changed everrrrrything because it automatically sorts a portion of my money (that i would’ve normally spent mindlessly) into savings. There is a low cost per month (like $3) to use the app, but alllll the money you effortlessly save pays for itself in a second. I am three years into using this app (do I sound hipster???) but it truly is WILD how quickly the money adds up. I truly consider this the most valuable app I’ve ever invested in, and I can’t wait for you to try it!

The best part? If you set up your account now with this link, you get anywhere from $5 to $25 fo’ free in your Qapital account (they change the bonus sign-on gift alllll the times but you’ll AT least get $5 if you use my referral link!) I smiled SOOOO big reading these. Here are some of my followers who have tried it! I love seeing ladies take charge of their finances. 👊🏽

There ya have it— the millennial’s guide to saving BIG for a down payment, wedding, ANYTHING. I’m by no means a financial guru or accountant—which is why I think you’ll like this savings plan. I’m just a normal gal with a normal paycheck trying to use my money to LIVE my life and invest in the things that matter. I hope this post inspires you to assess your finances, prioritize your spending, and START SAVING. You’ve got this, girlfriend!

As always—let me know if you have any questions in the comment section below! I’m here to help ya, friend. :)

didya like this post? here are some more you’ll love: